5 September, 2023

Top 5 Hydrocarbon Accounting Issues

What are the most important things to get right for an effective hydrocarbon accounting system? Here’s our list.

We will explore each hydrocarbon accounting issue in more detail in the next few weeks. Stay tuned!

1. One version of the truth

There should be a single database containing the definitive set of production data for the organisation. This database should be the source of all production reports used internally or distributed externally to partners and regulators.

Failure to achieve this leads to silos of production data being maintained by departments or individuals. This in turn causes conflicting data to appear, resulting in uncertainty, lack of confidence in the data and inefficiency as effort is spent reconciling differences.

2. Data integrity

The ability to correct errors in metering data is a key function of any hydrocarbon accounting system. But if corrections are not controlled, integrity is lost, leading to inconsistencies between input data and the calculated results that are based on those inputs.

Data integrity can only be ensured by applying effective controls within the hydrocarbon accounting system, including approval and locking of input data; indicating results that are out of date; and maintaining versions of all data. These controls provide protection against the situations that lead to loss of data integrity.

3. Transparency and auditability

Hydrocarbon accounting systems are relied upon to generate outputs that are often highly commercially sensitive, including partner allocations and production volumes reported to investors and regulators. It must be possible to verify this data, so there is no doubt about its correctness. This requires full transparency and auditability throughout the hydrocarbon accounting process.

Corrections made without an accompanying comment to explain the reason, and “black box” calculations that generate results without showing the intermediate steps, are the main causes of loss of auditability and transparency. This means results cannot be traced all the way through the process and therefore it is impossible to be certain they are correct.

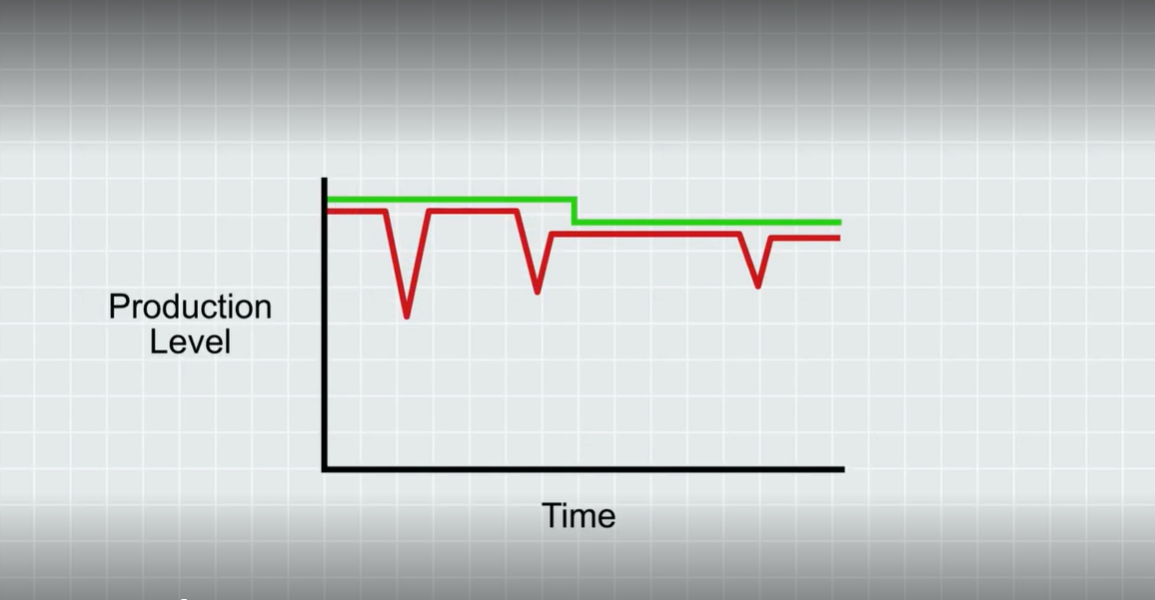

4. Input data validation

Most day-to-day issues in hydrocarbon accounting are caused by errors in input data. Given that the occurrence of some errors is inevitable, a good system must be able to detect errors reliably, deal with them consistently, and provide effective feedback to minimise recurrence.

Identifying incorrect data requires a combination of automatic and manual validation. Automatic validation is a valuable tool that can save time and improve reliability, but it depends on effective validation rules that must be regularly reassessed. Having identified errors in data received from metering or sampling systems, it is important that they are fed back to allow identification of cause.

5. Efficiency and reliability

The hydrocarbon accounting process is a continuous daily cycle. Issues that arise must be dealt with promptly, on the same day wherever possible. Failure to do so means the focus is on dealing with issues in previous cycles, leaving less time available for the current cycle. This is an environment in which errors are more likely to pass through undetected.

This situation can only be avoided if the process is efficient and the hydrocarbon accounting system does not require excessive user time and effort. An efficient and reliable system not only reduces direct costs, it also has indirect benefits, by making more time available to concentrate on ensuring high quality results.

Search

Other Resources

Uncertainty based allocation

Emissions Reporting in Axis

Production losses

Services